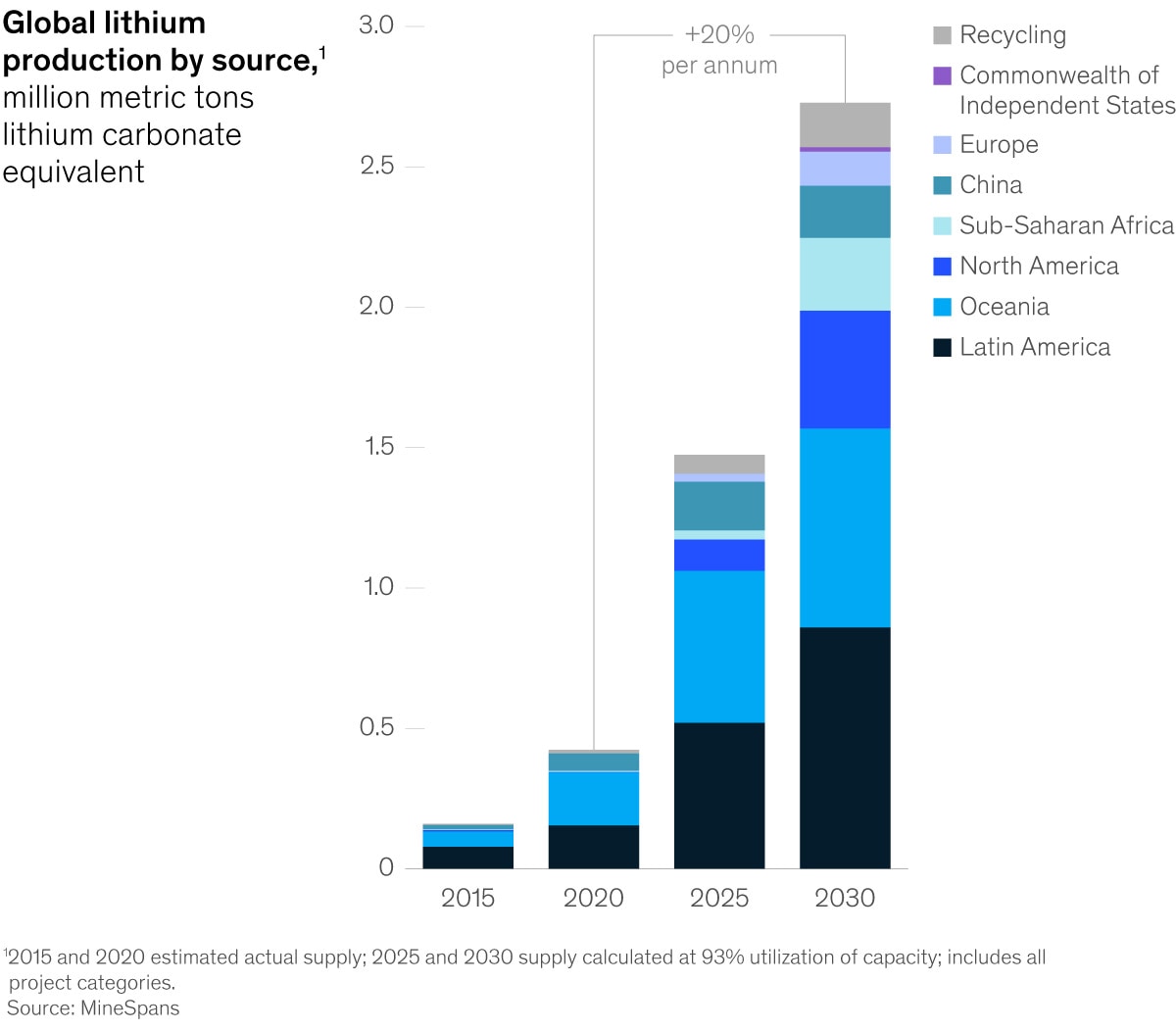

| Our best ideas, quick and curated | June 3, 2022 | | This week, we look at why high quit rates for nurses may imperil high-quality healthcare. Plus, new sources of lithium mining can help keep the electric-vehicle market moving, and how the war in Ukraine has caused 12 disruptions around the world. | | | | | Care crisis. If you or a loved one have ever spent time in a hospital, you know the power of nurses to provide expertise and give comfort. But who is giving comfort to nurses, whose ranks have been stretched thin throughout the COVID-19 crisis? Over the past two years, McKinsey has found that nurses consistently, and increasingly, report planning to leave the workforce at rates higher than in the past decade. | | Supply–demand imbalance. Before the pandemic, the number of new nursing licenses in the US continued to grow at around 4 percent per year, infusing the nursing workforce with fresh talent to replace those who retired. In the latest McKinsey survey of healthcare professionals, 29 percent of registered nurses in the US (consistent with numbers in France, Japan, Singapore, and the UK) indicated that they were likely to leave their current role in direct patient care, with many saying they intended to leave the workforce entirely. This attrition rate, while bad for the nursing profession, also has broad implications for the overall US healthcare sector, which is already grappling with the challenges of caring for an aging population with an increasing number of chronic care needs. | | A growing gap. Earlier in 2022, 90 percent of COVID-19 Hospital Insights Survey respondents said workforce shortages were a barrier to addressing the increasing elective-surgery volume, up 11 percentage points from 2021. By 2025, McKinsey estimates that the US may have a gap of between 200,000 to 450,000 nurses available for direct patient care, equating to a 10 to 20 percent gap. To meet this demand, the US would need more than double the number of new graduates entering and staying in the nursing workforce every year for the next three years straight. | | Support on the front lines. While nurses respond to compensation as a factor in remaining in their positions, they say doing meaningful work is crucial. Factors such as feeling engaged by work and maintaining good health are also top drivers in surveyed nurses’ decisions to stay. What else would retain nurses? A McKinsey Frontline Workforce Survey in March 2022 revealed that nurses who had left direct patient care said a more manageable workload, increased total compensation, ability to take time off, and being more valued by an organization would be the most important factors they would consider when evaluating a return. | | There is no one-size-fits-all solution to the challenges of being a nurse. However, key stakeholders, such as healthcare providers, could focus on leadership support and better workforce planning and deployment. Positive leadership initiatives—such as directors doing rounds to show their support—have been correlated with higher retention, reduced medical errors, and administrative efficiency. If no actions are taken, there will be more patients in the US who will need care than there will be nurses available to deliver it. That’s a position that benefits no one. In the long run, investing in nurses is also an investment in patient care. | | |  | | OFF THE CHARTS | | Minding the gap in the lithium-mining map | | Lithium is the driving force behind electric vehicles, but will its supply keep pace with demand? New technologies and sources of supply can fill the gap. Currently, almost all lithium mining occurs in Australia, China, and Latin America, which account for a combined 98 percent of production in 2020. An announced pipeline of projects will likely introduce new players and geographies to the lithium-mining map. This reported capacity base should be enough for supply to grow at a 20 percent annual rate to reach over 2.7 million metric tons of lithium carbonate equivalent by 2030. | | | | | | | | | | INTERVIEW | | Approach every situation with ‘a learner’s humility’ | | When Arundhati Bhattacharya retired as chairwoman of the State Bank of India in 2017, many observers thought her corporate journey had reached its end. But a few years into retirement, Bhattacharya became the CEO of Salesforce, India. Her move marked the beginning of a new professional chapter on several fronts: a shift from the public sector to the private sector, from banking to technology, and from a legacy Indian institution to an American software company. Yet, Bhattacharya has always believed that lifelong learning is the key to success. “When I think of the future, I see people having multiple careers,” she told McKinsey in a recent interview. “People will have to unlearn, relearn, and be on a learning curve for a very long time—in fact, for as long as they work.” | | | | | | MORE ON MCKINSEY.COM | | War in Ukraine | Twelve disruptions from the war in Ukraine are affecting people’s lives and livelihoods with potent force, and they should be part of every company’s scenario planning. The longer the war lasts, the more unpredictable such disruptions may become. | | State of fashion technology | As technological innovation accelerates, fashion companies can focus on harnessing technology to creativity, streamlining operations, and creating value from innovation that can be sustained in the years ahead. | | Addressing Europe’s corporate and technology gap | How can European countries tackle long-standing gaps in corporate performance and innovation? The answers lie in focusing on innovation in detail and in practice, technology by technology and sector by sector. | | | | | | | TECH FOR EXECS | | Get your head in the cloud’s services: SaaS, PaaS, and IaaS | | McKinsey experts serve up a periodic look at the technology concepts that leaders need to understand to help their organizations grow and thrive in the digital age. | | What they are. Virtually every aspect of IT can now be leased as a service (aaS) via the internet from a host of providers. Cloud service providers, in particular, have expanded rapidly into the aaS world. Rather than having to buy, install, and manage an application, you can simply use it when you need it and let the provider handle the maintenance. These services change the face of IT costs, capabilities, speed, and responsiveness. Businesses can now access and begin using applications in as little as a few hours and avoid significant up-front investments in technology infrastructure that can quickly become obsolete. | | But the space has become an alphabet soup. SaaS (software as a service), PaaS (platform as a service), and IaaS (infrastructure as a service) are at the forefront of aaS offerings, leaving business executives scratching their heads over the differences among them—and which would best enable businesses to achieve their goals. We’re here to help make sense of it all. | | SaaS benefits. SaaS providers lease business software (for instance, customer-relationship-management systems like Salesforce, file managers like Box, and messaging systems like Slack) on a subscription basis, allowing for quick scaling and the flexibility to use the software only as long as needed. SaaS enables businesses to practically eliminate the costs of developing and maintaining applications on site. Quick and simple access to applications from any device can speed adoption and use and can increase worker productivity. | | SaaS limitations. SaaS software can be customized to a certain degree. However, the ability to innovate at the speed of markets means that businesses will likely need to up their technology innovation game beyond what SaaS providers were designed to provide. | | PaaS cloud service. Designed to support businesses’ need for in-house development capabilities without requiring reversion to significant IT infrastructure or new talent investments (such as SAP Cloud or Google App Engine), PaaS offers online access to servers, data centers, middleware, and software development and project management tools. Like with SaaS offerings, the pay-as-you-go structure allows companies to scale up or down almost instantly as markets or customer expectations change. PaaS can significantly accelerate a company’s time to market; businesses that have adopted it report bringing new capabilities to market around 20 to 40 percent faster than do companies that haven’t. Organizations can also lift and shift legacy applications to a PaaS so that they can retire server farms and reduce software license expenses. | | IaaS access. IaaS has swooped in to offer virtual access to computing, storage, and networking resources (for example, Amazon Web Services and Microsoft Azure) so that businesses will not have to return to buying hardware to support all their new applications and tooling. IaaS providers enable businesses to increase or decrease capacity as needed, serving as a particularly valuable resource for data management and compute power, especially if the volume is soaring or unpredictable. | | Minding the economic pitfalls. These aaS offerings are by no means plug and play. Shifting to the cloud requires executives to carefully consider how these services support strategy and mesh with each other and existing IT hardware. Some companies have made costly mistakes when dealing with the economics of cloud services, often because business leaders try to apply old-school, on-site computing economics to them. McKinsey’s cloud calculator is one tool that can help you determine the right strategy for aaS offerings. | | What technology concepts would you like us to help explain next? Let us know. | | | — Edited by Barbara Tierney | | | Share this Tech For Execs |  |  |  | | | | | | BACKTALK | | Have feedback or other ideas? We’d love to hear from you. | | | | | | This email contains information about McKinsey’s research, insights, services, or events. By opening our emails or clicking on links, you agree to our use of cookies and web tracking technology. For more information on how we use and protect your information, please review our privacy policy. | | You received this email because you subscribed to The Shortlist newsletter. | | | | Copyright © 2022 | McKinsey & Company, 3 World Trade Center, 175 Greenwich Street, New York, NY 10007 | | | |

No comments:

Post a Comment